Simplified taxation system - deadlines for submitting reports. LLC reporting on the simplified tax system: what reports are submitted using the simplified system

Simplified accounting and reporting are not related to taxation. It can be conducted by companies both using the simplified tax system and other modes, including the general one. This opportunity is provided to small businesses, non-profit organizations (except for foreign agents) and Skolkovo participants. In the article we will answer the question of whether it is necessary to submit the balance sheet of an LLC under the simplified tax system in 2019, as well as individual entrepreneurs and non-profit organizations.

The simplified requirements for legal entities are stricter: among other things, the value of their depreciable fixed assets on the balance sheet cannot exceed 100 million rubles.

The balance sheet for an LLC using the simplified tax system for 2019 can be drawn up according to the simplified scheme provided for by Federal Law No. 402 and By Order of the Ministry of Finance dated July 2, 2010 No. 66n. However, the detail of reporting is left to the discretion of the LLC: full and short versions are acceptable. What balance does the LLC submit to the simplified tax system? Read about it below.

Annual form for individual entrepreneurs and LLCs on the simplified tax system: what balance to submit for 2019

A regular 3-page report with numerous attachments or a simplified 2-page report with explanations if necessary (for example, in case of losses)? Depending on the type of activity of the organization and the accounting accounts it uses: if rare accounts are used that are not in the short form of the report, then it is better to use the full version. For companies engaged in such common activities as trade, transportation or construction, the lightweight version of the form reflects the results of financial activities quite fully.

Do I need to report to individual entrepreneurs using a simplified form? Not necessarily, but if you wish, you can prepare reports in any form based on the data in the income (and expenses) ledger.

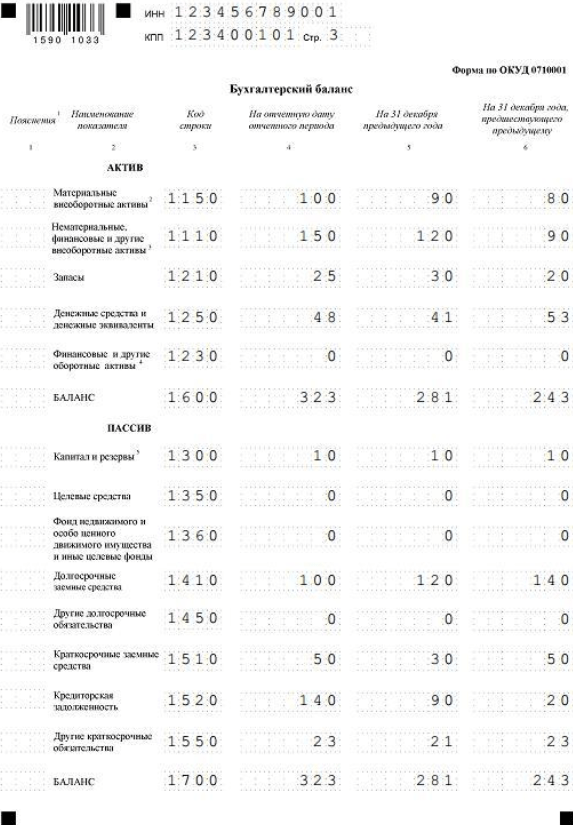

Is it possible for NPOs to report in a simplified manner? Yes, instead of a report on financial results, NPOs fill out a simplified report on the use of targeted funds. The lightweight version is much shorter. You can see how to correctly fill out the balance sheet of an NPO using the simplified tax system in the example (Fig. 1).

How to make a simplified balance sheet for the simplified tax system for 2019: form and recommendations

First you need to close the accounting reporting period. To balance the balance, accounts 90, 91 and 99 are closed on December 31 of the reporting year - this is called reformation. For a simplified balance sheet under the simplified tax system in 2019, this procedure is the same as for a regular one. The necessary transactions are presented in the table; an example of filling out a statement of financial results based on these transactions is shown in Fig. 2. For such entities, subaccounts for value added tax and excise taxes (90-3, 90-4, 91-3) are irrelevant.

Table. Postings during the reformation.

Simplified financial statements: example of filling

Rice. 1. Example of an income statement for 2019

Before drawing up a balance sheet under the simplified tax system in 2019, download the form - for example, in the appendix to the article. Data can be entered into forms manually, on a computer, or automatically through an accounting program.

The balance under the simplified tax system for 2019 had to be submitted on March 31. Since in 2019 it is a day off - Sunday, it will need to be submitted by 04/01/2019. Simplified companies do not report quarterly, and in the full version, the balance sheet is submitted only for the year.

Financial statements must be submitted to the Federal Tax Service and Rosstat (together with statistical ones). For some organizations, accounting data is public, for example for non-profit organizations, and they are required to be published in a printed publication. However, most ordinary organizations are not subject to this requirement.

Step-by-step filling out the balance under the simplified tax system for 2019

The information on the first two pages of the new simplified financial statements for 2019 should contain all information about the organization and summary accounting data.

Rice. 2. “Descriptive” pages of financial statements.

Drawing up a balance sheet under the simplified tax system for 2019 implies only 5 types of assets and 8 types of liabilities (Fig. 1). Passive accounts have been detailed compared to the previous form. Two added items - “targeted funds” and “fund of real estate and especially valuable movable property” - are necessary to detail the organization’s assets. They need to indicate data on targeted funds aimed at major repairs, modernization of fixed assets or innovation. In addition, many organizations will be required to record the value of real estate or vehicles on their balance sheet.

Please note: the line code corresponds to the account that has the greatest share of it. For example, an enterprise has intangible assets worth 100 thousand rubles. (code 1110) and financial investments worth 50 thousand rubles. (code 1170). In the report, in the line “Intangible, financial and other non-current assets”, code 1110 will be indicated, but the total amount will be entered - 150 thousand rubles. - on both counts.

The company's income is shown in the income statement (Fig. 2). It is filled out along with a simplified balance sheet in a simplified manner in 2019, also known as Form 2, profit and loss statement.

Sample of a finished balance sheet under the simplified tax system in 2019

Simplified financial statements of a profitable company for 2019 (full set, thousand rubles).

Financial statements of an unprofitable company (USN “income minus expenses”). An example of filling out a balance sheet under the simplified tax system “income minus expenses” (Form 2) with a loss is slightly different from the “profitable” option. There are no differences in the LLC balance sheet under the simplified tax system for 2019.

Be prepared to provide explanations to tax inspectors in case of losses. You can immediately issue an explanatory note about the reasons for their occurrence. Enterprises and individual entrepreneurs using the simplified regime are not required to compile it in full. Losses can be explained by writing off overdue accounts receivable, etc. Tax officials can also clarify your intentions to correct the situation.

We remind you that an organization can switch to a simplified tax system by sending a notification to the Tax Service. The article on our portal will help you do this.

The most important annual report of any simplified company is a declaration under the simplified tax system. The form, the electronic format and rules for submission of which were approved by order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3/99@. We'll tell you how to fill out the document correctly.

It is no coincidence that the simplified tax regime is so named. Taxes that are difficult to calculate, such as VAT, income tax and property tax, are generally not paid by simplifiers and do not submit appropriate declarations. All these taxes are combined for them into a single simplified tax. However, based on the results of 2018, companies using the simplified tax system need to be prepared to provide a considerable amount of other information, which we will discuss in today’s article.

A declaration on the simplified tax system for organizations and individual entrepreneurs is available in the BukhSoft program. The report is always on an up-to-date form, taking into account all changes in the law. The program will fill out the form automatically. All you have to do is download it. Before sending to the tax office, the declaration is tested by all verification programs of the Federal Tax Service. Try it for free:

Declaration under simplified tax system online

Declaration under the simplified tax system for 2018

The most important annual report of any simplified company is a declaration under the simplified tax system. The form, electronic format and rules for submitting the declaration were approved by order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3/99@. The deadline for submitting a simplified declaration for legal entities is (the deadline has been postponed, since 03/31/2018 is Sunday).

Declarations under the simplified tax system are submitted by companies that use the simplified tax system both with the object “income” and with the object “income minus expenses.” A declaration under the simplified tax system is always submitted, even if no activity was carried out during the year. In the latter case, you need to submit a zero form to the tax authorities on the same form as a regular completed declaration.

Information can be submitted to tax authorities in three ways:

- bring it on paper in person to the Federal Tax Service at the place of registration;

- on paper, send by registered mail;

- transmit in electronic format via TKS.

The easiest and most convenient way to submit information is electronically through an EDF operator.

Annual reporting 2018 simplified tax system to the Tax Inspectorate

We have collected for you all the simplified tax reports for 2018 in one table, which you can view below.

|

Type of information |

When to serve |

Method of submitting information |

Document approving the form |

useful links |

| Transport tax return for 2018 | If vehicles are registered with a legal entity no later than February 1, 2019 | Order of the Federal Tax Service of Russia dated December 5, 2016 No. ММВ-7-21/668 | Answers to questions about transport tax | |

| Land tax return for 2018 | If there are land plots owned by the legal entity no later than February 1, 2019 | On paper. Electronically (required for employees over 100 people) | Order of the Federal Tax Service of Russia dated May 10, 2017 No. ММВ-7-21/347 | How to generate a land tax return in accounting software Bukhsoft |

| VAT return for the 4th quarter of 2018 | If in the 4th quarter of 2018 the taxpayer issued invoices using the simplified tax system with allocated VAT or was a tax agent with the responsibilities specified in Art. 161 Tax Code of the Russian Federation. No later than January 25, 2019 |

Only electronically (exception - VAT tax agents) |

Order of the Federal Tax Service of Russia dated December 20, 2016 No. ММВ-7-3/696 | How to fill out sections of the VAT return in Bukhsoft programs Fill out explanations for VAT in Bukhsoft Online |

| Income tax return for 2018 | When a company receives profit under the simplified tax system from foreign organizations controlled by it, from dividends and interest received from certain securities (clause 2 of article 346.11 of the Tax Code of the Russian Federation). No later than March 28, 2019 | On paper. Electronically (required for employees over 100 people) | Order of the Federal Tax Service of Russia dated October 19, 2016 No. ММВ-7-3/572@ | |

| Property tax return for 2018 | When owning real estate, the tax base for which is determined as its cadastral value (clause 2 of Article 346.11, Article 378.2 of the Tax Code of the Russian Federation). When owning residential premises that are not taken into account on the balance sheet as the main asset of the company under the simplified tax system. No later than April 1, 2019 | On paper. Electronically (required for employees over 100 people) | Order of the Federal Tax Service of Russia dated March 31, 2017 No. ММВ-7-21/271@ | How to correct errors in property calculations in the Bukhsoft accounting program? |

| Information on the average number of employees for 2018 | No later than January 21, 2019 (the deadline has been postponed because January 20 is Sunday) | On paper. Electronically (required for employees over 100 people) | Order of the Federal Tax Service of Russia dated March 29, 2007 No. MM-3-25/174@ | How to fill out information about the average headcount in the accounting program |

| Report on form 6-NDFL for 2018 | No later than April 1, 2019 | Order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/450 | ||

| Certificate in form 2-NDFL for 2018 | No later than April 1, 2019 | On paper. Electronically (required for employees over 25 people) | Order of the Federal Tax Service of Russia dated October 30, 2015 No. ММВ-7-11/485@ | |

| Balance sheet | No later than April 1, 2019 (the deadline has been postponed because March 31 is Sunday). Companies on the simplified tax system submit only a balance sheet without reporting on financial activities, only if it does not contain information without which an objective assessment of the financial condition of the organization is impossible | Electronically | Order of the Federal Tax Service of Russia dated March 20, 2017 No. ММВ-7-6/228@ | Simplified accounting (financial) reporting in the Bukhsoft program |

| Declaration on UTII for the 4th quarter of 2018 | When combining simplified taxation system and UTII. No later than January 21, 2019 (the deadline has been postponed because January 20 is Sunday) | On paper. Electronically (required for employees over 100 people) | Order of the Federal Tax Service of Russia dated October 19, 2016 No. ММВ-7-3/574@ |

For many entrepreneurs who have registered as an individual entrepreneur or LLC and have chosen the simplified tax system, an acute question arises: what papers (reports, declarations, calculations, etc.) and when should I submit? Requirements are constantly changing, let's try to figure out what and when needs to be passed to simplifiers in 2018.

Questions of this nature and many others, businessmen have long been accustomed to solving in this service, try it to minimize risks and save time.

Reporting the simplified tax system to the tax office

Let's start with the most declarations according to the simplified tax system, which is filled out for the past year. Its due date for LLCs and individual entrepreneurs is different: for legal entities it is March 31, for individual entrepreneurs the deadline is a month longer, that is, April 30. Before this date, you must submit a paper declaration in person (or through a representative), by mail or in electronic format. It is not recommended to delay this until the last day - you may be late, and through no fault of your own.

What else are we renting? Declarations for other taxes:

- for transport and land They must be submitted by February 1st. The requirement applies only to organizations, so they calculate the tax themselves. You can choose the document delivery format - paper or electronic. Individual entrepreneurs are individuals, so the inspectorate considers these taxes for them.

- UTII declaration- relevant for those who combine two special regimes and, accordingly, must submit two declarations - both simplified and UTII. The declaration is filled out quarterly, you can also choose the form of submission, the deadlines are set for the 20th of January, April, July and October.

- if you have been recognized as a property tax payer since 2015(from which the tax is now paid from the cadastral value), then within 30 days after the end of the quarter you need to submit a tax calculation (since advance payments are paid for the tax). This requirement is also relevant only for legal entities, since LLCs must calculate the tax themselves.

- VAT declaration must be filled out only by those who pay it. Yes, the simplification provides for exemption from VAT, but there are certain cases when it is still required to pay, which means you need to report. The deadline for submission from 2015 is set on the 25th day of the month following the completed quarter (January, April, July and October, respectively). The declaration is submitted only electronically.

What about information related to existing staff?

By January 20, data on the average number of employees must be submitted to the inspectorate. For organizations this requirement is mandatory; for individual entrepreneurs the situation is somewhat different. If you are an individual entrepreneur with employees, you also rent, but if you don’t have them, you don’t need to rent. But there are times when you don’t currently have employees, but you hired them for a certain period of the year, for example, 2-3 months. In this case, information must be submitted, even if the figure is rounded to zero. If the tax office has questions, you will simply need to prepare an explanation.

Those who act as tax agents and withhold personal income tax from their employees need to submit two more documents: a certificate (by April 1) and a message about the impossibility of withholding personal income tax, if such facts exist (by March 1). In addition, starting from 2016, you also have to submit 6-NDFL - a month after the end of the quarter is given for submitting the report, and the report for the year must be submitted before April 1.

Since 2017, employers have quarterly reported to the tax office on insurance premiums - they submit. The deadline for its submission is set at the 30th day of the month following the completed period.

If the number of employees exceeds 25 people, you are required to submit these forms in electronic format.

For organizations using the simplified form, they must submit annual financial statements to the tax authorities. The deadline is set at March 31 (three months after the end of the reporting period).

Reporting of the simplified tax system to funds

Three reports must be submitted to the funds: , and SZV-STAZH with the general form EDV-1 (data on the number of employees). 4-FSS is submitted quarterly, SZV-M - monthly, and information about insurance experience - annually. The deadlines are set as follows:

- 4-FSS in paper format must be submitted by the 20th day of the month following the end of the quarter, in electronic format - by the 25th day of the same month.

- RSV-1 in paper form must be submitted by the 15th day of the month following the quarter, in electronic form - by the 20th day.

- SZV-M must be submitted by the 15th day of the month following the reporting month.

Information about the insurance experience must be submitted before March 1 of the next year, that is, for 2017, this report must be submitted before March 1, 2018.

When these dates fall on the weekend, they are also transferred to the next day - Monday. Please note a very important point: since 2015, the requirements for submitting these documents electronically have changed. The report is submitted to the Social Insurance Fund in electronic format if the number exceeds 25 people, to the Pension Fund - 25 or more. If there are fewer employees, then you can choose the form of delivery.

All LLCs and individual entrepreneurs who are registered as an employer report, even if you worked alone during the reporting period. Individual entrepreneurs without employees who pay a fixed rate of contributions for themselves do not need to hand over anything.

What other documents need to be submitted to government agencies?

Such documents include reporting to Rosprirodnadzor and statistical authorities.

A Declaration of Fee for Negative Impact on the Environment must be submitted to Rosprirodnadzor - this should be done only when, according to the law, you are recognized as a payer of the environmental fee. The declaration must be submitted by March 10 of the year following the expired period. If the specified date falls on a weekend, the deadline for submitting the report is postponed to the next working day. The new type of report must be submitted in electronic format, certified by an electronic signature. In paper form, this declaration can be accepted by those who, firstly, do not have an electronic signature, secondly, the annual fee for negative impact on the environment is equal to or less than 25 thousand rubles, and thirdly there is no connection to the Internet due to technical problems.

What do we include in statistics? Firstly, LLCs using the simplified tax system must submit their financial statements to the statistical authorities. The deadline is March 31st. Secondly, simplified LLCs and individual entrepreneurs must submit special statistical reporting:

- form No. PM is submitted by small enterprises (no later than the 29th day of the month following the reporting quarter);

- Form No. MP (micro) is submitted by microenterprises, except those engaged in agriculture (the form is annual, it must be submitted by February 5);

- Form No. 1-IP is filled out by individual entrepreneurs not employed in agriculture (the form is also filled out for the year, submitted by March 2).

For some types of activities (trade, agriculture), Rosstat provides special forms of statistical observation.

Not everyone needs to submit statistical reporting, but only those LLCs and individual entrepreneurs that were included in the sample of the territorial statistics body. You should receive the corresponding official requirement from the statistical authority. To know for sure whether you will need to submit something to the statistical authorities this year or not, it is best to contact the territorial authorities at the place of registration. Information about those included in the sample can also be found on the Rosstat website.

Popular and convenient, as well as significantly reducing the amount of taxes payable, the simplified taxation scheme is used by most companies that fall under the criteria for using the simplified tax system. Let's consider what kind of reporting LLCs are required to submit to the regulatory authorities using the simplified tax system.

LLC reports under the simplified tax system

The simplified tax system combines two different taxation options that differ in the size of the tax rate, calculation base and calculation procedure:

- STS “Income”, where all income received during the reporting period is taxed, without taking into account the costs incurred. The marginal tax rate is 6%, but regional authorities are given the right to reduce it to 1%. If there is no income, no tax is charged.

- STS “Income minus expenses”, when the tax base is the difference between the income of the reporting period and the expenses incurred in it. The tax rate varies from 5 to 15% and is also set by the constituent entities of the Russian Federation. An important aspect in this regime is the mandatory accounting of costs and their compliance with the list of expenses of the Tax Code of the Russian Federation, which can be taken into account when calculating the tax base.

LLC reporting on the simplified tax system is the same for both types of “simplified” and consists of:

- tax reporting - declaration according to the simplified tax system;

- accounting - annual balance sheet, profit and loss statement, appendices and explanations thereto;

- monthly and quarterly (personnel reports to the Federal Tax Service, Pension Fund and Social Insurance Fund).

LLC reporting on the simplified tax system to the Federal Tax Service and extra-budgetary funds

“Simplified” reporting to the Federal Tax Service is presented in one annual form - a declaration according to the simplified tax system. There are no intermediate forms for “simplified” students. Calculations of quarterly advances paid are not prepared in separate reports, but are taken into account in the annual declaration. The current declaration form in 2018 was approved by Federal Tax Service Order No. ММВ-7-3/99 dated 02/26/2016 - the same for all “simplified” payers, regardless of the tax objects used (they only fill out different sheets in the report). The information that is entered in the declaration is initially accumulated in the tax register - KUDiR.

In addition to the declaration, once a year they submit to the Federal Tax Service information on the average number of employees and data on personnel income (2-NDFL certificates), as well as a balance sheet with all appendices and an explanatory note.

Companies are also required to report quarterly, providing:

- in the Federal Tax Service - a unified calculation of insurance premiums and Calculation 6-NDFL;

- in the FSS - report 4-FSS on “injuries”.

To the Pension Fund of the Russian Federation, “simplified” employees submit information about insured employees every month (form SZV-M), and at the end of the year - forms SZV-STAZH and EDV-1.

Accounting statements of LLC on the simplified tax system

Despite the term “simplified”, which has come into common use, there are no exceptions for companies using the simplified tax system in terms of accounting, which means that all of them must keep full records and promptly (within 90 days after the end of the year) submit the appropriate reports to the Federal Tax Service . The company's accounting policy regulates and establishes accounting criteria, which determines whether the company will maintain a full or simplified version of accounting.

Small and micro enterprises are allowed not to use registers used in standard accounting methods: they have the right to keep books of registration of facts of economic activity. Both versions of accounting and reporting (full and simplified) are contained in Order of the Ministry of Finance of the Russian Federation No. 66n dated July 2, 2010.

Deadlines for submitting LLC reports to the simplified tax system

Let's group the necessary reports and deadlines for their submission in the table:

|

Frequency and deadlines for delivery |

||||||||

|

Declaration according to the simplified tax system |

||||||||

|

Balance Sheet and Attached Forms |

||||||||

|

For the year, no later than April 1 (certificates with attribute “1”), or no later than March 1 (certificates with attribute “2”) of the year following the reporting year |

||||||||

|

Information on the average number of employees |

||||||||

|

Quarterly, until the end of the month following the reporting quarter, for the year - until April 1 of the following year |

||||||||

|

Calculation of insurance premiums |

Quarterly, no later than the 30th day of the month following the reporting quarter |

|||||||

|

Monthly, no later than the 15th day of the month following the reporting month |

||||||||

|

SZV-STAZH and ODV-1 |

||||||||

|

Quarterly, no later than the 20th (on paper) or 25th (electronically) of the month following the quarter |

LLC reporting on the simplified tax system without employees

The absence of employees (and even production activity) does not exempt the LLC from submitting reports - in such situations, zero reporting is provided. Organizations submit within the established deadlines:

- to the Federal Tax Service - a declaration according to the simplified tax system and annual accounting records, as well as information on the average number of employees; submit quarterly a zero form of calculation for insurance premiums;

- in the FSS - report 4-FSS and confirmation of the main type of activity;

- in the Pension Fund of the Russian Federation - monthly forms SZV-M and annual forms SZV-STAZH and ODV-1 for the head of the company, incl. if he is its founder, with whom an employment contract has not been concluded.

Thus, permission to implement a simplified tax regime for a company does not mean that the legislator will weaken monitoring of the functioning of “simplified” companies. This is manifested by setting strict deadlines for submitting mandatory reports to all regulatory authorities. Failure to comply with the reporting calendar for LLCs on the simplified tax system established by law will certainly entail penalties.